Biodiversity reporting frameworks: A comparative guide for responsible organisations

This article is available in french here.

With the environmental crisis and the acceleration of international regulations, companies are increasingly under scrutiny for their impact on nature. To guide their transparency and actions, several reporting frameworks are emerging, playing a central role in corporate strategies. In 2023, we explored the initial implications of the CSRD directive; more than a year later, it’s time to review its implementation and the challenges it poses for organizations.

In this article, we compare three major initiatives that are redefining the relationship between businesses and biodiversity: the CSRD, the TNFD, and the SBTN. While their approaches differ, these initiatives are complementary and fit within the broader framework of climate and environmental reporting.

The CSRD: A European regulatory framework with a specific standard dedicated to biodiversity

The Corporate Sustainability Reporting Directive (CSRD) is a European directive developed by the European Financial Reporting Advisory Group (EFRAG). It requires certain companies to publish detailed reports on their sustainability efforts. The CSRD replaces the Non-Financial Reporting Directive (NFRD) and aims to ensure transparency, consistency, and comparability of sustainability data across companies.

Who is currently affected?

Standardized Reporting through ESRS

The CSRD relies on the European Sustainability Reporting Standards (ESRS), which comprise 12 standards covering four main areas:

Each standard is detailed in a document called a "delegated act" and consists of:

• The objectives of the standard;

• Disclosure requirements (strategy, risk and opportunity management, indicators);

• Application requirements.

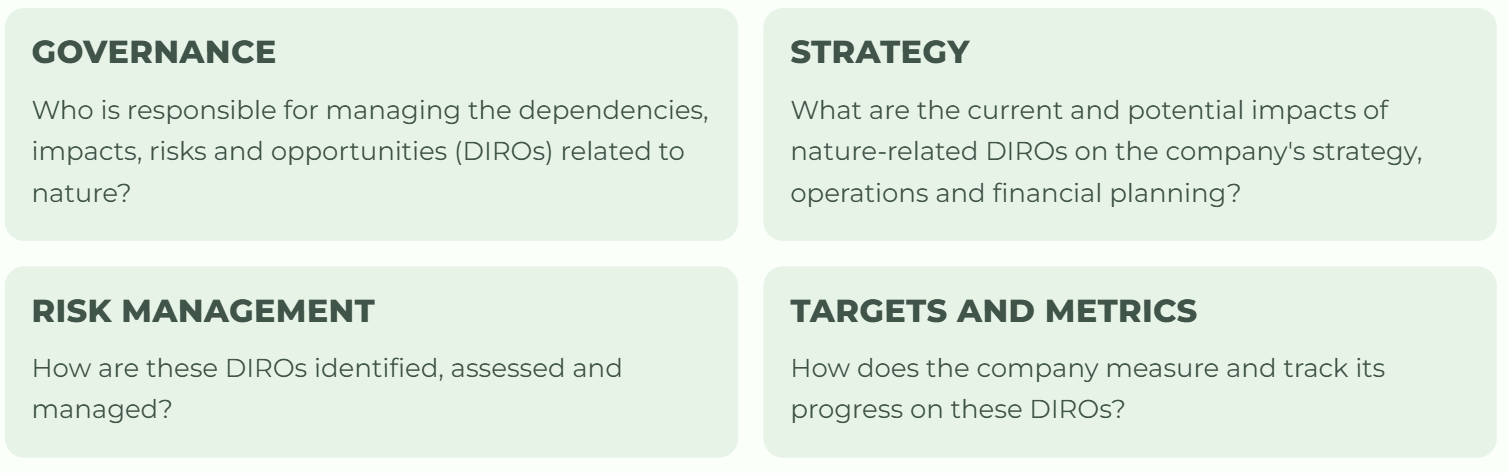

The disclosure requirements of ESRS E4: Biodiversity and Ecosystems are explained in this article. To summarize, they cover the analysis of dependencies, impacts, risks, and opportunities related to nature. It also requires companies to provide detailed information about their policies, actions implemented and planned, targets to be achieved, indicators to be monitored, and financial effects related to these dependencies, impacts, risks, and opportunities (DIROs).

The CSRD thus establishes a mandatory framework but allows companies the flexibility to use other tools, such as the TNFD or SBTN, to go further.

The TNFD: A Voluntary Framework Focused on Assessment and Disclosure

The Taskforce on Nature-related Financial Disclosures (TNFD) is a voluntary initiative launched in 2021 by the UN, UNEP, and various governments. It provides recommendations to help companies understand and communicate their interactions with nature.

Who is concerned?

Initially designed for financial institutions, the TNFD’s disclosure recommendations now target organizations of all sizes and sectors.

These recommendations are relevant to a broad range of stakeholders: businesses, investors, financial institutions, rating agencies, and financial service providers.

TNFD Recommendations

The TNFD framework is based on 14 disclosure recommendations grouped into four themes:

A Clear Methodology: LEAP

The TNFD offers a methodology called LEAP to guide companies in their reporting:

Locate: Identify interactions with nature.

Evaluate: Assess impacts and dependencies.

Assess: Analyze risks and opportunities.

Prepare: Prepare disclosures.

This framework also provides biome- and sector-specific guidance, allowing for tailored solutions to meet each company’s needs.

The SBTN: A Voluntary Framework Focused on Action

The Science Based Targets for Nature (SBTN) differs from the other two by its focus on driving companies to take concrete actions to reduce their impact on nature. It is supported by a consortium of organizations (WWF, CDP, UNEP-WCMC, Global Compact, WEF, WRI, etc.).

Who is concerned?

The SBTN framework primarily targets businesses and organizations seeking to measure, reduce, and restore their impact on nature using a science-based approach aligned with global sustainability goals. It also provides ambitious tools for transforming business models to better respect planetary boundaries.

A Five-Step Methodology

The SBTN follows a structured approach:

Tools to Guide Action

The SBTN promotes the use of tools such as life cycle analysis (LCA) and databases like Global Forest Watch (GFW) to support decision-making.

Differences and Complementarities Between CSRD, TNFD, and SBTN

These three frameworks are complementary, and your choice depends on your organization’s level of maturity. In any case, they share common principles:

An approach based on the five pressures identified by IPBES to quantify biodiversity impacts.

A comprehensive consideration of the entire value chain.

An initial materiality assessment to identify priority sites and key company activities.

A "double materiality" approach that accounts for both financial materiality (nature’s impact on a company) and impact materiality (a company’s impact on nature), enabling the evaluation of dependencies, impacts, risks, and opportunities (DIRO).

A vision of biodiversity that encompasses ecosystem integrity and species extinction risk.

The inclusion of site-specific information in assessments (local evaluation).

Active collaboration with stakeholders and local communities.

In summary, if you are subject to the CSRD, the TNFD and SBTN methodologies can enhance your approach by going beyond minimum requirements. For companies looking to transform their strategy, the SBTN offers a unique opportunity to move from reflection to action.

At Natural Solutions, we are here to help you navigate this ever-evolving landscape. By leveraging the power of data and AI, we can assist you in selecting the most relevant indicators for your business, as well as in building and managing your biodiversity data effectively, regardless of the framework you choose.